Revenue looks good on paper.

The sales dashboard is green. New contracts are signed. Distributors are ordering. Production is running. The board sees growth.

But behind the scenes, the finance team is under pressure.

Payroll is approaching. Raw material suppliers are asking for payment. The factory needs working capital to keep moving. Yet a large portion of “revenue” is still sitting inside unpaid invoices.

This is one of the biggest hidden problems in manufacturing:

A company can be profitable on paper and still suffer from cash flow pressure in reality.

For many manufacturers, especially those selling to B2B distributors, a sale is not truly complete when goods are shipped. It is only complete when cash enters the bank account.

And that can happen 30, 60, 90 days later—or even later than promised.

In today’s environment, where working capital is expensive, supply chains are tight, and business uncertainty remains high, waiting for invoices to become overdue is no longer good enough.

Manufacturers need to move from reactive collection to predictive cash flow intelligence.

This is where machine learning can create a very real business impact.

—

The Problem with Traditional Cash Flow Forecasting

Most companies still forecast cash flow using fixed payment terms.

If the invoice says 30 days, they assume payment will arrive in 30 days.

If the invoice says 60 days, they assume payment will arrive in 60 days.

But in real business operations, this is often not what happens.

Some distributors always pay late. Some delay payment only when invoice value is large. Some slow down payments near their own quarter-end. Some use payment delays as a way to preserve their own working capital. Others delay because of operational issues such as shipment disputes, wrong documentation, pricing mismatches, or quality claims.

The problem is that traditional finance reporting often hides these patterns.

A metric like Days Sales Outstanding may tell management the average collection period. But average numbers can be dangerous.

A company may have an average DSO of 45 days, but that average may hide a serious problem: several large distributors may be consistently paying after 75 or 90 days.

On paper, the average still looks manageable.

In reality, the company may be carrying a liquidity risk.

This is why finance leaders need to look beyond average numbers. They need invoice-level visibility. They need distributor-level behavior analysis. They need to know which invoices are likely to be delayed before the delay happens.

—

Late Payment Is Not Always an Accident

In B2B distribution, late payment is not always caused by financial difficulty.

Sometimes, it is a strategy.

A distributor may delay payment to improve their own working capital position. They may use the manufacturer as a source of short-term financing. They may stretch payment terms because they know the supplier wants to protect the business relationship.

This creates a difficult situation for manufacturers.

Sales wants to maintain the relationship.

Finance wants to protect cash.

Operations needs certainty to plan production.

Management needs visibility to decide whether to extend credit, pause shipment, offer discounts, or escalate collection.

Without good data, these decisions become subjective.

With machine learning, the company can start identifying payment behavior patterns objectively.

—

What Machine Learning Can Detect

Machine learning can help manufacturers analyze historical and operational signals that human teams may not easily see.

For example, the model can analyze questions such as:

Does this distributor always pay late after a certain invoice size?

Do they pay slower near month-end or quarter-end?

Do they delay payment when shipments are partially fulfilled?

Do quality claims increase the chance of delayed payment?

Do portal login patterns indicate whether the invoice has been reviewed?

Do certain regions, product lines, or sales teams have higher collection risk?

Do late payments increase when interest rates rise or when the distributor’s market is under pressure?

This is where the power of machine learning becomes useful.

It does not only look at accounting data. It can combine data from ERP, warehouse systems, manufacturing systems, customer portals, logistics systems, and external market indicators.

That is the difference between a basic finance report and a predictive cash flow system.

—

From Static Forecast to Probabilistic Cash Flow

A traditional cash flow forecast says:

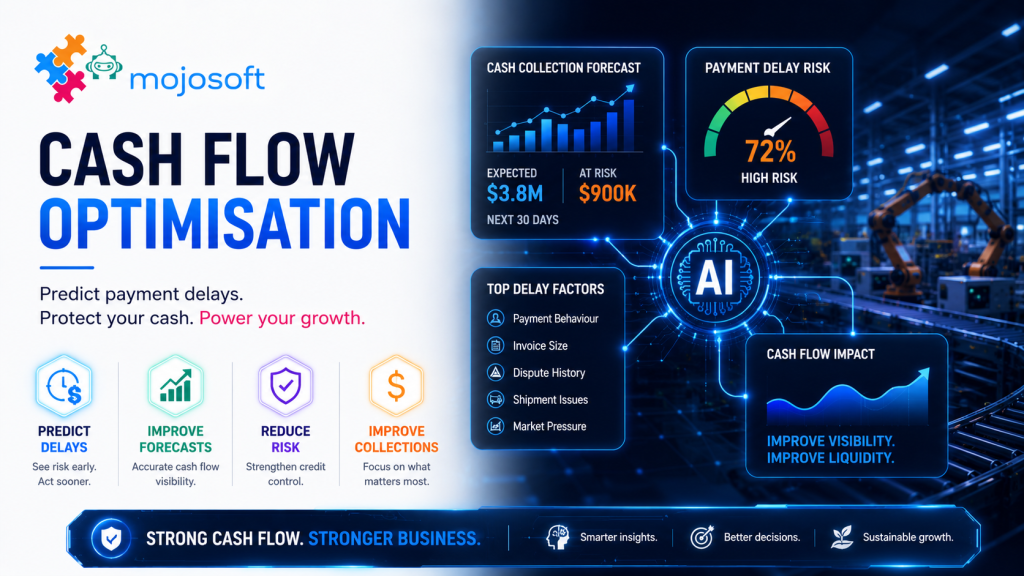

“We expect to receive $5 million next month.”

A predictive cash flow system says:

“We have $5 million in invoices due next month, but based on distributor behavior, dispute signals, invoice size, shipment history, and payment pattern, the expected cash collection is closer to $3.8 million. Another $900,000 has a high probability of being delayed by more than 15 days.”

This is a completely different level of management visibility.

It allows the CFO to make decisions earlier.

It allows treasury to plan funding more accurately.

It allows sales to intervene before a customer becomes overdue.

It allows operations to avoid committing too much production capacity to high-risk customers.

Most importantly, it reduces surprises.

In business, the problem is often not that payment is late.

The bigger problem is that management only finds out too late.

—

Practical Use Cases for Manufacturers

A machine learning-based payment delay prediction system can support several practical business use cases.

### 1. Prioritised Collection

Instead of calling customers only after invoices are overdue, the system can identify high-risk invoices before the due date.

Collection teams can focus on the accounts that matter most.

High-value, high-risk invoices can be escalated earlier. Low-risk customers can receive automated reminders. This makes collection more strategic and less reactive.

### 2. Better Cash Flow Forecasting

Management can forecast cash inflow based on probability, not just due date.

This helps reduce the gap between projected cash and actual cash.

For manufacturers with heavy raw material purchasing, labour cost, and production commitments, this visibility is critical.

### 3. Dynamic Credit Control

The system can help identify distributors whose payment behavior is deteriorating.

Instead of reviewing credit limits once or twice a year, companies can adjust risk exposure dynamically.

A distributor with worsening payment behavior may require tighter shipment controls, revised credit limits, partial prepayment, or management review.

### 4. Smarter Invoice Factoring

Not all invoices need to be factored.

With predictive analytics, a manufacturer can selectively factor only the invoices that are likely to create liquidity pressure.

This avoids unnecessary factoring cost on healthy receivables and improves working capital efficiency.

### 5. Early Dispute Detection

Many payment delays are caused by operational friction: wrong price, incomplete document, shipment issue, or quality claim.

If these signals can be detected early from ERP, WMS, MES, or customer portal data, the company can resolve the issue before the invoice becomes overdue.

—

Why This Matters to the CFO

For the CFO, this is not merely an analytics project.

It is a working capital optimisation initiative.

The ability to predict payment delays can directly impact:

Cash flow accuracy

Borrowing cost

Working capital requirement

Customer credit risk

Collection productivity

Production planning

Supplier payment confidence

Board-level financial visibility

In many companies, millions of dollars are trapped in inefficient receivables management.

The company may be borrowing money while its own cash is stuck in overdue invoices.

That is an expensive problem.

By improving payment prediction and collection prioritisation, manufacturers can reduce unnecessary borrowing, improve liquidity planning, and unlock cash that is already inside the business.

—

Why This Matters to Sales and Operations

This is also not only a finance problem.

Sales teams need visibility because payment behavior affects customer quality.

Not every large customer is a good customer. A distributor that places big orders but consistently delays payment can quietly damage the manufacturer’s cash position.

Operations teams also need visibility because production planning depends on financial reliability.

If a distributor has growing unpaid invoices and increasing payment delay risk, the company may need to review whether future shipments should continue without intervention.

The goal is not to damage customer relationships.

The goal is to manage them with better intelligence.

Good customers should be supported.

Risky customers should be managed more carefully.

And high-value customers with temporary payment issues should be handled proactively before the issue becomes a crisis.

—

The Data Foundation Is Critical

Of course, machine learning does not work well if the underlying data is poor.

To build this capability, manufacturers need to connect and clean data from multiple systems:

ERP for invoices, credit terms, payment history, and customer master data

CRM for sales activities and customer relationship signals

WMS and logistics systems for shipment status and delivery exceptions

MES or production systems for quality issues, batch problems, and fulfilment delays

Customer portals for invoice viewing, dispute submission, and document download activity

External data sources for market, interest rate, regional, or industry pressure

This is why data governance matters.

If customer names are inconsistent, invoice records are incomplete, payment dates are inaccurate, and operational events are not properly captured, the model will not perform well.

AI does not magically fix poor data discipline.

It amplifies the quality of the data foundation.

—

The Real Transformation: From Collection to Prevention

The biggest shift is mindset.

Traditional accounts receivable management asks:

“Who has not paid us yet?”

Predictive cash flow management asks:

“Who is likely not to pay us on time, and what can we do before that happens?”

That is the transformation.

It moves the company from chasing overdue invoices to preventing cash flow disruption.

It moves the CFO from backward-looking reporting to forward-looking decision-making.

It moves the business from reactive collection to proactive liquidity control.

For manufacturers, this can become a competitive advantage.

Because the companies that manage cash better can buy raw materials with more confidence, invest in automation faster, negotiate better with suppliers, and withstand market shocks more effectively.

—

Conclusion: Cash Flow Intelligence Is Becoming a Management Necessity

In manufacturing, cash flow is not just a finance metric.

It is operational fuel.

A factory can have strong sales, modern machines, and a growing customer base. But if cash collection is unpredictable, the business remains exposed.

Machine learning gives manufacturers a better way to understand payment behavior, predict delay risk, and act before problems become visible in the bank account.

The future of accounts receivable is not only about sending reminders and chasing overdue invoices.

It is about building an intelligent cash flow engine that can predict, prioritise, and protect liquidity.

For manufacturing leaders, the message is clear:

Revenue growth is important. But predictable cash flow is what keeps the business alive.